Medicare Insurance

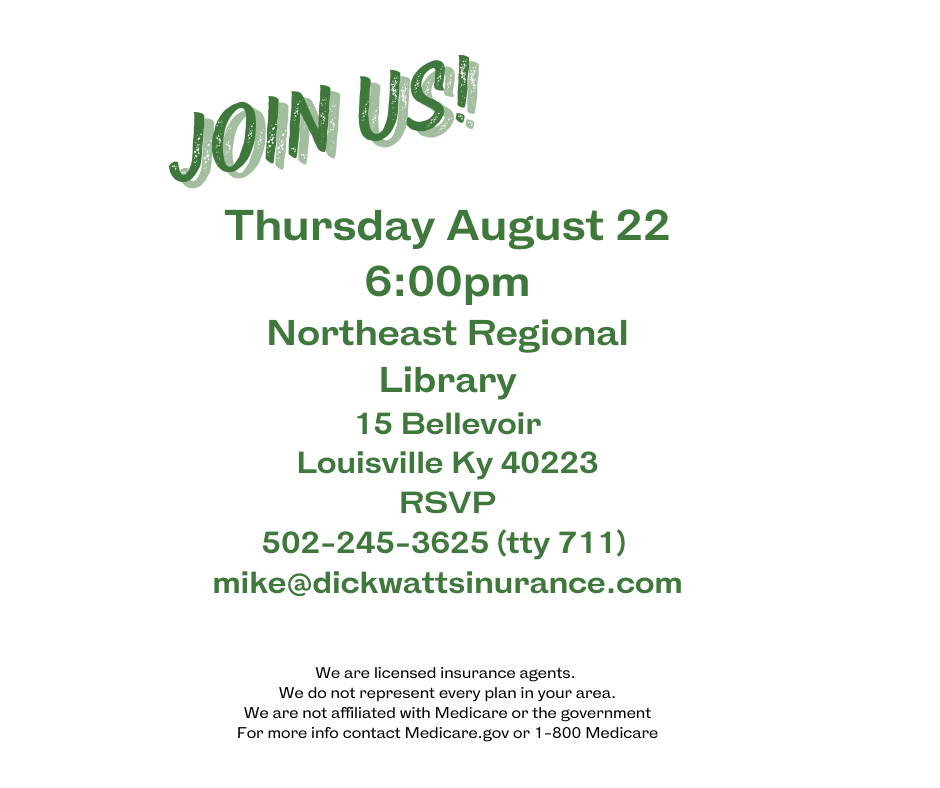

RESERVATIONS FORM FOR NEXT MEDICARE 101 ON AUGUST 22ND

RSVP FOR MEDICARE 101

RSVP FOR MEDICARE 101

Understanding Medicare: A Comprehensive Guide for Seniors

Navigating the world of Medicare can seem overwhelming, but it’s essential to understand your options to make the best choices for your health and budget. This guide breaks down the basics of Medicare, its various parts, and how you can maximize your benefits.

What is Medicare?

Medicare is a federal health insurance program designed primarily for individuals aged 65 and older. It also covers some younger individuals with disabilities and those with End-Stage Renal Disease (ESRD).

The Parts of Medicare

Medicare is divided into different parts, each covering specific services:

Medicare Part A: Hospital Insurance

- Coverage: Inpatient hospital stays, skilled nursing facility care, hospice care, and some home health care.

- Cost: Most people don’t pay a premium for Part A if they or their spouse paid Medicare taxes while working. However, there are deductibles and coinsurance.

Medicare Part B: Medical Insurance

- Coverage: Outpatient care, preventive services, doctor visits, and some home health services.

- Cost: Part B requires a monthly premium. There is also an annual deductible and coinsurance, typically 20% of the Medicare-approved amount for services after the deductible is met.

Medicare Part C: Medicare Advantage

- Coverage: An alternative to Original Medicare (Parts A and B) offered by private companies approved by Medicare. These plans often include additional benefits such as vision, dental, and hearing, and most include prescription drug coverage.

- Cost: Varies by plan. You still pay the Part B premium, and there may be additional premiums, deductibles, and copayments.

Medicare Part D: Prescription Drug Coverage

- Coverage: Helps cover the cost of prescription drugs. Part D plans are offered by private insurance companies approved by Medicare.

- Cost: Monthly premium, annual deductible, and copayments or coinsurance. Costs vary by plan and income level.

Enrollment Periods

Knowing when to enroll in Medicare is crucial to avoid late enrollment penalties:

Initial Enrollment Period (IEP):

- Starts three months before you turn 65, includes your birthday month, and ends three months after your birthday month (a total of seven months).

General Enrollment Period (GEP):

- If you miss your IEP, you can enroll between January 1 and March 31 each year, with coverage starting on July 1. Late enrollment penalties may apply.

Special Enrollment Period (SEP):

- You may qualify for a SEP if you have certain life events, such as losing employer coverage or moving out of your plan’s service area.

Medicare Advantage Open Enrollment Period:

- From January 1 to March 31, you can switch Medicare Advantage plans or return to Original Medicare.

Understanding Costs

Premiums: Regular payments to maintain your coverage.

Deductibles: The amount you pay out-of-pocket before Medicare starts to pay.

Copayments and Coinsurance: Your share of the costs for services after meeting your deductible.

Supplemental Insurance: Medigap

Medigap Plans:

- These are additional policies sold by private companies to cover gaps in Original Medicare, such as copayments, coinsurance, and deductibles.

- Different Medigap plans offer different levels of coverage and are standardized by the federal government.

Tips for Choosing the Right Plan

- Assess Your Health Needs: Consider your current health status, medications, and any anticipated medical needs.

- Compare Costs: Look at premiums, deductibles, and out-of-pocket limits.

- Check Provider Networks: Ensure your preferred doctors and hospitals are covered by the plan.

- Evaluate Additional Benefits: Look for plans offering extra benefits that are important to you, such as dental, vision, or wellness programs.

- Seek Assistance: Use resources like the State Health Insurance Assistance Program (SHIP) for free, unbiased help.

Maximizing Your Medicare Benefits

- Preventive Services: Take advantage of free preventive services covered under Medicare Part B, including screenings, vaccinations, and annual wellness visits.

- Medication Management: Use the Medicare Plan Finder tool to compare Part D plans and find one that covers your prescriptions at the lowest cost.

- Stay Informed: Review the “Medicare & You” handbook each year to stay updated on changes to coverage and costs.

Additional Resources

- Medicare.gov: The official U.S. government site for Medicare.

- 1-800-MEDICARE: Call for personalized assistance.

- State Health Insurance Assistance Program (SHIP): Offers free, local counseling.

Understanding Medicare is key to making informed decisions about your healthcare. By familiarizing yourself with the different parts of Medicare, enrollment periods, and the costs involved, you can choose the plan that best meets your needs and ensures you receive the care you deserve.

We are licensed insurance agents.

We do not offer every plan available in your area. Currently we represent 5 organizations which offer 26 health plans in your area.

You can always contact Medicare.gov, 1-800-MEDICARE, or your local State Health Insurance Program (SHIP) for help with plan choices

Ready to Start Your Quotes?

We make the process super easy. When you’re ready, click the button below to see how we can help you!

Have a great experience

Online review help our agency tremendously. If you’ve had a good experience, we’d love your review!